The Smart Money’s Playbook: Buying at the 52-Week Low and Selling at the 52-Week High

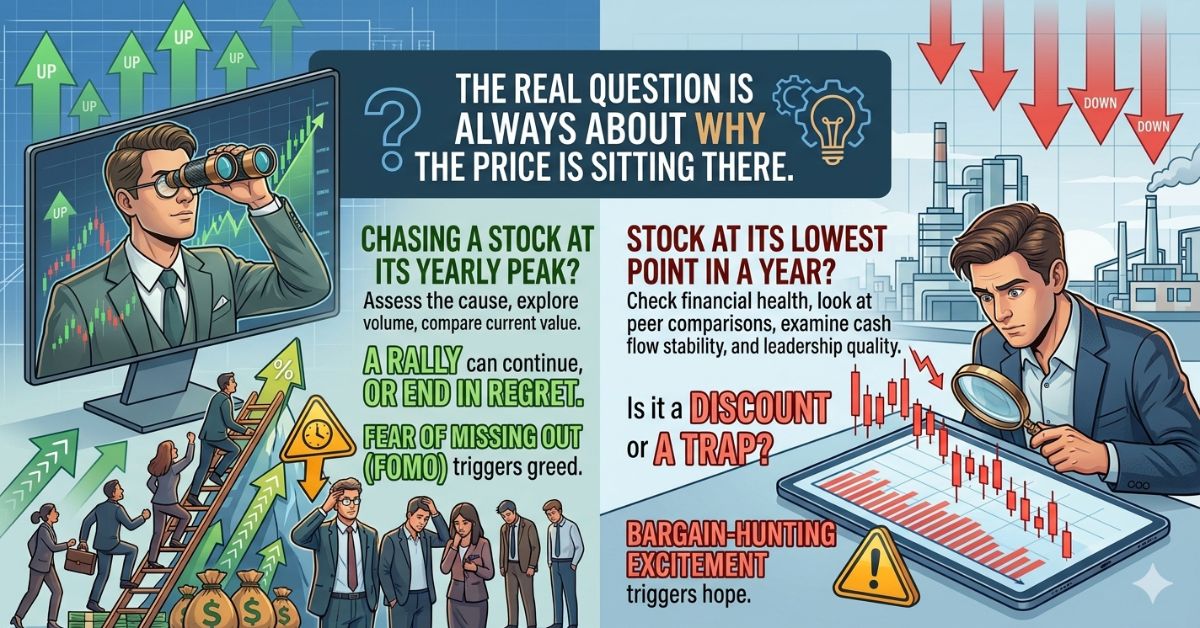

An investor is looking at a stock that recently hit its highest price in a year and thinking if there’s still time to buy. Somewhere else, another investor is looking at a company trading at a level it has not sunk to in a year and debating whether that is a golden opportunity or a warning sign. Both of these investors are asking the wrong question. The real question is never about where the price is sitting. It is always about why the price is sitting there.

Lists of 52 weeks high stocks and 52 weeks low shares are among the most visited sections on the NSE and BSE portals every single trading day. They attract eyeballs because extreme numbers trigger strong emotions. A yearly high sparks greed, and a yearly low sparks either fear or bargain-hunting excitement. But the investors who actually make money from these lists are the ones who refuse to let either emotion drive the final call.

Chasing a Stock at Its Yearly Peak Has a Funny Way of Turning Confidence Into Regret

There is an uncomfortable truth that nobody on financial social media likes to admit. Most retail participants who buy 52 weeks high stocks enter the trade after the significant move has already happened. They see a name climbing aggressively, read a few optimistic posts online, and convince themselves that the rally is just getting started. Sometimes they are right. A stock breaking into new yearly territory on the back of outstanding quarterly earnings, genuine institutional accumulation, and improving sector fundamentals can absolutely continue its upward journey. But a stock that reached the same level on thin trading volume, speculative chatter, and no meaningful change in the underlying business is a completely different animal. The second situation frequently ends in a dramatic turnaround that severely penalises late arrivals. Before allowing excitement to transfer into real capital placement, successful investors assess the cause behind the breakout, explore whether volume supports the strength of the move, and compare the current value versus industry peers.

A Stock Sitting at Its Lowest Point in a Year Deserves Curiosity, Not an Automatic Buy Order

The 52 weeks low list carries its own unique psychological trap. Value investors look at deeply discounted prices and feel an almost magnetic pull toward buying. The reasoning feels logical on the surface because purchasing a stock at its cheapest point in a year seems like common sense. Except common sense without context is just guesswork dressed in comfortable clothing. Companies land at yearly lows for wildly different reasons. Some fall because the entire market is under pressure and even healthy businesses get dragged down alongside weaker ones. Others fall because their revenue is declining, their debt is ballooning, their management is losing credibility, or their sector is facing structural challenges that are not going away anytime soon. Anand Rathi share and stock broker equips investors with research tools that allow them to dig beneath the surface of these price drops by examining financial health, peer comparisons, cash flow stability, and leadership quality before deciding whether a low price represents a discount worth taking or a trap worth avoiding entirely.

Yearly Extremes Are Signposts on the Road, Not Destinations Where Investors Should Park Blindly

The fundamental mistake that keeps repeating itself across market cycles is treating the 52 weeks high stocks list and the 52 weeks low list as ready-made shopping guides. They were never designed to serve that purpose. These lists reflect where prices have traveled over the past year, not where they are heading next. A stock at its peak could double from there if the business supports it, or it could collapse under the weight of overvaluation. A stock at its floor could bounce back beautifully, or it could sink further into territory that makes the current low look generous by comparison.

The Investors Who Win Consistently Are the Ones Who Treat Data as a Starting Line, Never a Finish Line

Price extremes open doors to better questions. Smart participants walk through those doors with research in hand and emotions left firmly outside.